02.24.26

How to Switch Phone Carriers

by Kathy Hinson

A spending plan doesn't have to be elaborate. This step-by-step guide will help you master your finances.

We talk a lot about saving money. Like, a lot. It’s on our website, on our socials, on our app. It’s what every reviewer talks about, every publication, every person that recommends TextNow to a friend or family member. We believe that an essential like a phone shouldn't cost anywhere near the $141 that JD Power lists as the average single-line cost — that's why TextNow offers service starting at $0.

But your money saving journey doesn’t have to end there. We work closely with personal finance experts to build our own guide on how to budget, just for you.

Here's your step-by-step guide to learn budgeting basics, make a budgeting plan, and save money.

Start with the basics: figuring out how much you’re actually spending every month. These numbers will fluctuate month by month, so it’s best to look back at a six-month period to get a reasonably complete picture.

To make your budgeting easier, split up your expenses into “fixed,” “fluctuating,” and “is it necessary?” categories:

A fixed expense is one that can't be avoided and is the same each month – rent or mortgage, insurance, internet, phone, transit pass, car, student loan payments, etc.

A fluctuating expense also can't be avoided, but the may vary. This includes things like utilities, groceries and household goods, gas, and credit card bills.

An "is it necessary" expense can be reduced or cut without significantly damaging your quality of life. This would include streaming subscriptions (can you do with one instead of three, or switch to a free ad-supported service?), takeout or delivery meals, coffee, entertainment, etc.

List the money coming in every month. If your job is salaried or you work guaranteed hours, this is an easy step. If that is not the case, then take an average of your last six months to get a baseline.

Now comes the part you’ve probably been dreading – figuring out how much of the money you’re bringing in is going out every month. But don’t worry, this number is just a starting point that will help you get on top of your finances.

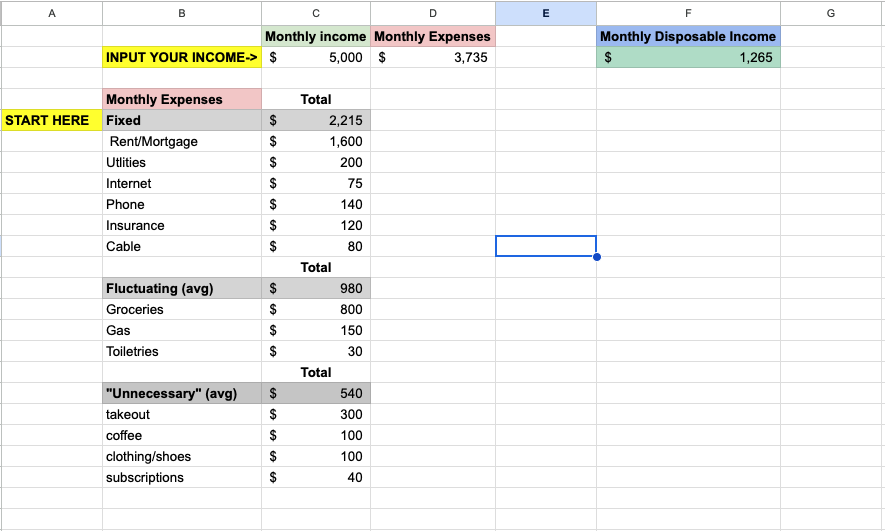

There are a lot of budget templates out there, some free, some paid, but you don’t need anything fancy to figure out how much you’re saving (or losing) every month. You can do the work with a free Google account and 30 minutes of your time. Use this simplified template we put together for an easy start and add/remove the expenses that actually apply.

*Disclaimer: the numbers listed are examples, please fill them with the actual numbers from your monthly statements.

The analysis you complete in step 3 will do this for you automatically, especially if you’re using the sample budget we provided.

This is a crucial step to starting your budget plan. Before you can move forward, it’s important to know whether you’re ending your months with extra money, running about even, or going into debt.

You probably went into this with some goals already in mind, and this is the time to get clear about what you’re trying to accomplish. There are two possible budgeting goals: Pay off debt and grow your savings.

If your goal is to pay off debt, whether it’s an existing lump sum (like a student or car loan), or a rolling monthly credit card debt, then here are a few tips that will help you pay off your debt efficiently:

Here are our tips for saving money with your new budget:

Put your saved money to work. Letting your money sit in a low-interest account will slow progress toward your overall goal. At the very least, open a high-yield savings account so your money earns more interest. But you should also consider investment options like a 401(k) account or a general investment account. There are plenty of options like ETFs that offer growth with lower risk than picking individual stocks. Contact your bank or other trusted institution for advice. Look for a fiduciary relationship, where the person or entity advising you is required to put your financial welfare ahead of their own benefit, such as commissions.

Now that you have a clear picture of your monthly expenses and how much you can save or pay off every month, it’s time to set yourself up for success and stay accountable.

Within the categories you created, set limits so that you don’t end up overspending. These could be monthly, weekly, or even daily spending caps. For example, if your goal is to cut your takeout expense so you have more money left over at the end of the month, set a specific spending limit so it’s not a vague “spend less” but a real number that you can track and stay within.

As we talked about in Step 1, you can start with a rough budget and refine later — the important thing is just getting started. As you get comfortable, dial in your budget with more precise numbers and take into account irregular expenses like taxes, car maintenance, gifts, etc.

Don't be afraid to adjust your goals, too. Seeing some progress can provide the inspiration you need to fuel more savings or debt paydown efforts.

If you have any questions, or want to share your own budgeting tips, send us a note at [email protected]!

Have questions or want to share your own budgeting tips? Send us a note at [email protected]!